For past half decade, the studio investment has been a trend in Japan. Those arrangers have acquired land on behalf of the potential investors, planed and developed the site as the studio apartment and sold them to the investors. Especially in Kyushu region, the Southern part of Japan, those service providers have been quit active.

Today, I would like to spend some time to analyze the profitability of those businesses, future prospects and feasibility as an investment sector.

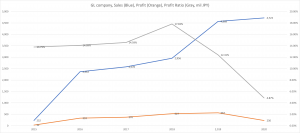

1 Players’ outline:

1 ) SK company, listed, based in Fukuoka, 950 mil USD sales, ca 85 mil USD profit, 8.92 % of profit ratio. They develop condominiums, which means a set of residential units for sale with strata ownership structure. Their targets are individual owners whose annual income is around 4 -7 mil JPY. SK develop condo, sell to investor, and on behalf of investors, they manage the unit in terms of leasing. At the end the yield remained to an owner would be roughly around lower than 5 percent.

2 ) GL company, listed, based in Kumamoto, 47 mil USD sales, 2.3 mil USD profit, the profit ratio is 4.8 %. Their clients are mainly doctors, wealthy individuals, or business owners. GL acquire the land, develops studio apartment building, sells the entire building to one owner. Their strength looks the planning ability: targeting high-end single residents in regional cities.

The strengths and weaknesses of this business model

1) Strengths

・ Meet the demand of the current market.

SK has been providing a investment product for individual office workers who have been under the pressure of building up their pension funds by themselves. In other words, under extremely low interest rate environment, SK has created investment product which seems to deliver at least above one percent of return. GL has been providing a good studio resident to fit as is Japanese society. Aged couples have been thinking of how to live after their partners’ passing away. Moreover, more and more singles in much younger generations say from twenties to forties. GL has created a decent living unit which satisfies those single residents.

・ Low development risk

In their scheme, developers have to have the cash to acquire the land to be developed. They don’t basically hold inventories or are never exposed to the development risks as the ownership of the products should be handed over t the investor, even under the development stage.

・Repeaters and words of mouths

Both scheme have been well supported by the market. The properties are brand new, after having a profit of several years, according to the advice proposed by the developer, who is called Asset Manager, clients sell the property. In addition to the proceeds, investors add some capital again, they re-invest in the new property investment developed by those players. The first-time investor looks so happy and he definitely show off their investment outcomes. This has been working to “seduce” new investors among their networks.

・Low land prices

The key of this scheme is prime location in the regional cities. This means seeking relatively low land price in a total development amount. This has supported those developers to acquire the lands with their full-equity scheme backed by corporate finance.

2) Weaknesses

・Vulnerable to market transition, low profit ratio

Obviously, the profitability ratio has been decreasing while the business volume has grown. There are several reasons to explain this declining profitability. High and aggressive acquisition, saturated demand in the local market, construction cost increase, the high fixed cost and weakened investment appetite under long lasting COVID pandemic. Especially, Japanese people have had high-preference in saving and the least desire to investment. Therefore, this kind of fundamental challenge has always undermined the investment scheme.

・Low investment incentives

As mentioned, now the investment return from the real estate doesn’t seem to match the risks involved in the product. In other words, there seem to be many other alternatives to obtain much higher investment return at lower risks. Therefore, those scheme seem to be sooner or later would become obsolete among potential investors.

・Vacancy risks

Moreover, the COVID has been bringing unexpected dynamism to the residential and office market in Japan. More and more people prefer working at home instead of spending long hours for commuting. We are not sure how the “ideal” living environment would be. On the other hand, it is really tough to convert designing, specifications and the fundamental structure of the apartment after its completion. Therefore, it is extremely challenging to anticipate the future trend which will be supported by single residents in the market after the COVID pandemic.

・Low profit margin

Both schemes have been generating profit through the apartment development. Especially, GL ‘s top leader is from architectural industry. He was believing that the cost management is one of their strength. However, for some specific markets where the supply and demand have been limited, the developers profit would be compressed by the increasing cost as well as pushed up land prices.

・End user’s liquidity

For instance, when it comes to sell the product to a doctor, under the COVID pandemic, the number of clinic clients has been decreasing. Some may consider giving up their operations. Others may consider hiding or diversifying their asset portfolio into real estate. Nevertheless, COVID has been so influential and has not allowed banks to provide much easier and favorable financial terms and conditions to the client.

・Market risks come from dynamic life style change

As mentioned above, now we are still uncertain how the aged people manage their lives after their retirements. Many single people, regardless of the gender, have been avoiding to live in a so-ccalled traditional one room studios. Therefore, at this moment, all we have to do is maintaining our positions while looking for new opportunities.

So, in a nutshell, those businesses have been supported by the market due to its uniqueness, market trend and and people’s interests.

I personally feel that it looks risky and not working well from now on. This model: developing a new studio apartment for investor, would sooner or later be automatically collapsed.

Further queries or doubts, please email to ytomizuka@abrilsjp.com

News Letter subscription is here

- Tags

- apartment, Fukuoka, investment, Japan, studio